More than 15 years after the introduction of the provision creating a two-tier special tax rate for retained profits of partnerships with balance sheets, the legislator is finally initiating the necessary reform. With the Corporate Tax Reform Act of 2008, the legislator wanted to introduce preferential treatment of retained profits for partnerships with the aim of "ensuring that high-earning and internationally competitive partnerships enjoy similarly favourable retention conditions as corporations." (cf. Draft law of the Federal Government of 18 May 2007, page 2 "Solution"). Hardly any partnerships utilised this provision, although successful (family-run) companies often do not distribute their profits for internal financing and development of their business activities. The biggest criticism of the previous regulation was in particular that non-deductible operating expenses, which a partnership could not in fact avoid (e.g. trade tax, income tax of the partners), were deemed to be withdrawals. Co-entrepreneurs of family-run partnerships often only have a right to withdraw tax on their respective income taxes payable under the partnership agreement, as these would otherwise reduce their assets outside the company. A liberal Ministry of Finance is now managing to make this regulation more practicable - a clear step towards tax optimisation.

The regulation

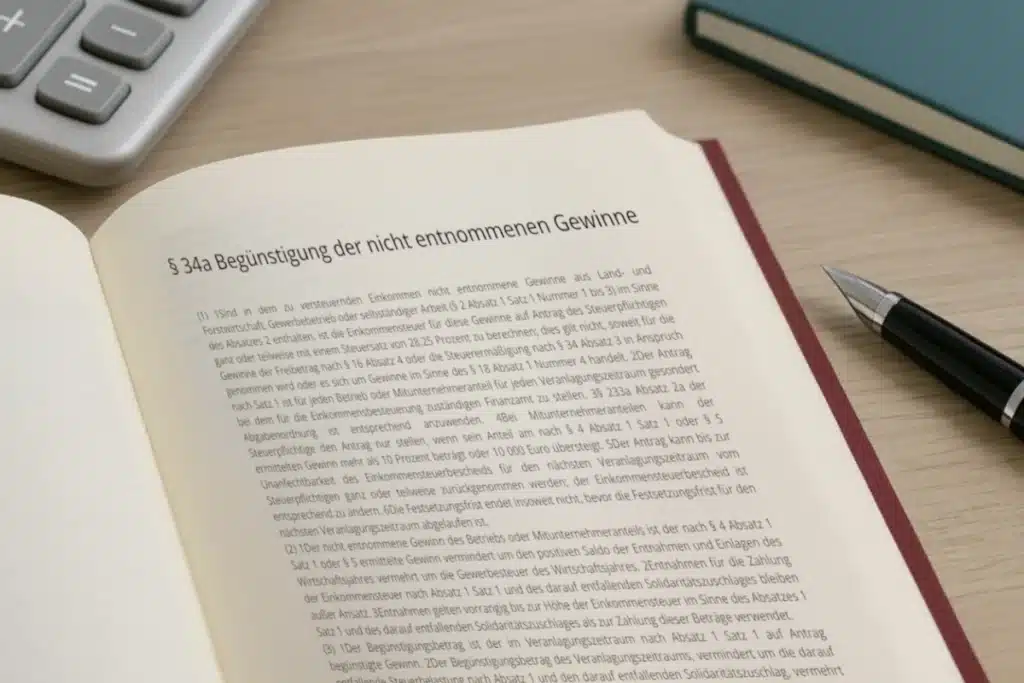

§ Section 34a EStG allows, among other things, co-entrepreneurs of partnerships with balance sheets to use a special rate for undrawn profits instead of the progressive income tax rate of 45 % plus solidarity surcharge. The profit not withdrawn is initially taxed at only 28.25 % plus solidarity surcharge. If preferentially taxed amounts are withdrawn at a later date, a further income tax of % plus solidarity surcharge is due. This creates new scope for tax optimisation within the framework of the Growth Opportunities Act.

The reform

The profit eligible for preferential treatment is now increased by the trade tax payable by the partnership. In addition, the partner's pro rata income tax including solidarity surcharge is not deemed to have been withdrawn. They therefore increase the profit eligible for tax relief. This means that a significantly higher retention volume will be available in future. The provision can be applied after Resolution of the Finance Committee of 15 November 2023, p. 37 can already be applied in the current 2024 financial year - a particular advantage for growth-oriented partnerships that focus on targeted tax optimisation.

Simple example

Family runs a successful company in the legal form of a KG. It generates a profit of 1,000k in the 2024 financial year. The partnership agreement stipulates that the partners may only withdraw a proportionate amount of income tax. The KG generates a pre-tax profit of K1,000, of which K860 could still be withdrawn after trade tax (ann. trade tax rate 14 %, assessment rate 400 %). The limited partnership posts these profits to the capital accounts and refunds the shareholders (ann. income tax rate 45 %) pro rata income tax of K310 after submission of the relevant notices. The KG therefore has K550 available for reinvestment under the current legal situation. If, on the other hand, the KG submits an application in accordance with Section 34a EStG (new version), it will have around K720 at its disposal, meaning that in future the retaining KG will have K31 1TP4 more capital available for further business development - a noticeable tax optimisation thanks to the Growth Opportunities Act.

The TAXGATE team and Dr Tobias Stiegler are at your side as experts in the tax-optimised design of your company structure - with a special focus on partnerships.